library(dplyr)

library(lmtest)

library(sandwich)

library(ggplot2)

library(fredr)

library(plotly)

library(zoo)LP Replication II

Simple replications of some Local Projections

Figure 5 of Local Projections: Jordà and Taylor (2024)

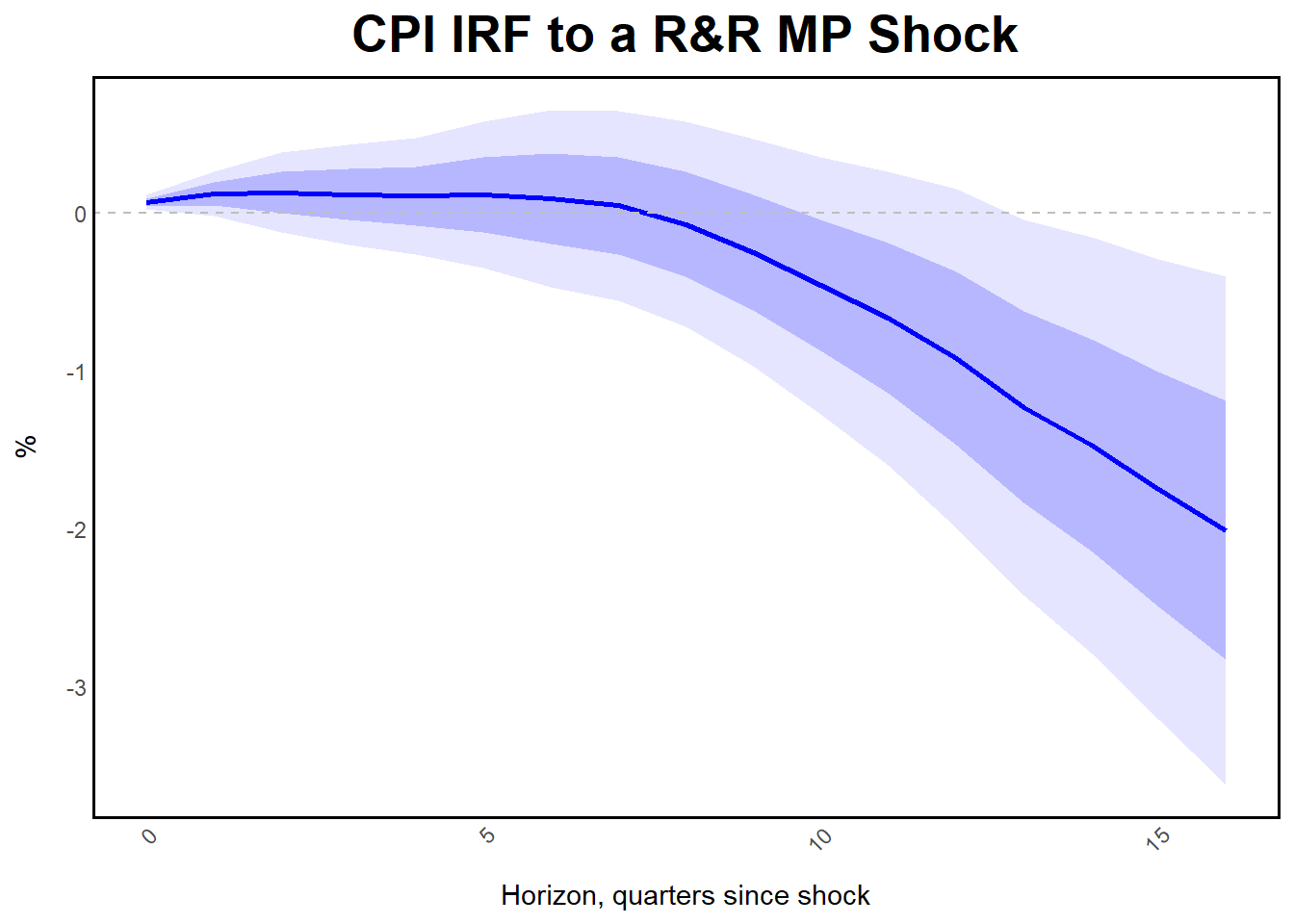

Another simple LP replication: this time, CPI Headline Inflation to a Romer&Romer shock whilst controlling by GDP and FedFunds

data <- haven::read_dta("aggregatedata_final.dta")

data <- data %>%

mutate(lcpi = 100 * lcpi,

lrgdp = 100 * lrgdp)

h <- 16

y <- "lcpi" # Response variable

z <- "rr_shock" # Instrument variable

nwlag <- h # N. of Newey-West lags

p <- 0.05 # Significance level

for (i in 0:h) {

data <- data %>%

mutate(!!paste0(y, "_f", i) := lead(!!sym(y), i) - lag(!!sym(y), 1))

}

results <- data.frame(

horizon = 0:h,

b = rep(NA, h + 1),

se = rep(NA, h + 1)

)

# LP Regressions

for (i in 0:h) {

formula <- as.formula(paste0(

y, "_f", i, " ~ ", z,

" + lag(dlrgdp, 1) + lag(dlrgdp, 2) + lag(dlrgdp, 3) + lag(dlrgdp, 4) ",

" + lag(dlcpi, 1) + lag(dlcpi, 2) + lag(dlcpi, 3) + lag(dlcpi, 4) ",

" + lag(stir, 1) + lag(stir, 2) + lag(stir, 3)+ lag(stir, 4)"))

model <- lm(formula, data = data)

nw_se <- coeftest(model, vcov = NeweyWest(model, lag = h, prewhite = FALSE))

results$b[i + 1] <- coef(model)[z]

results$se[i + 1] <- nw_se[z, 2]

}

results <- results %>%

mutate(

u1 = b + se,

d1 = b - se,

u2 = b + qnorm(1 - p / 2) * se,

d2 = b - qnorm(1 - p / 2) * se

)

ggplot(results, aes(x = horizon)) +

geom_ribbon(aes(ymin = d2, ymax = u2), fill = "blue", alpha = 0.1) + # 95% confidence band

geom_ribbon(aes(ymin = d1, ymax = u1), fill = "blue", alpha = 0.2) + # Standard error band

geom_line(aes(y = b), color = "blue", size = 1) + # Point estimate

geom_hline(yintercept = 0, linetype = "dashed", color = "gray") + # Zero line

labs(x = "Horizon, quarters since shock", y = "%", title = "CPI IRF to a R&R MP Shock") +

theme_minimal() +

theme(

plot.title = element_text(hjust = 0.5, size = 20, face = "bold"),

plot.subtitle = element_text(hjust = 0.5, size = 14, face = "italic", margin = margin(t = 10, b = 10)),

axis.text.x = element_text(angle = 45, hjust = 1),

panel.grid.major = element_blank(),

panel.grid.minor = element_blank(),

panel.border = element_rect(color = "black", fill = NA, size = 1),

axis.line = element_blank(),

axis.ticks.length = unit(-0.25, "cm"),

axis.title.x = element_text(margin = margin(t = 10)),

axis.title.y = element_text(margin = margin(r = 10)),

legend.position = "top",

legend.title = element_blank(),

legend.text = element_text(size = 12)

)

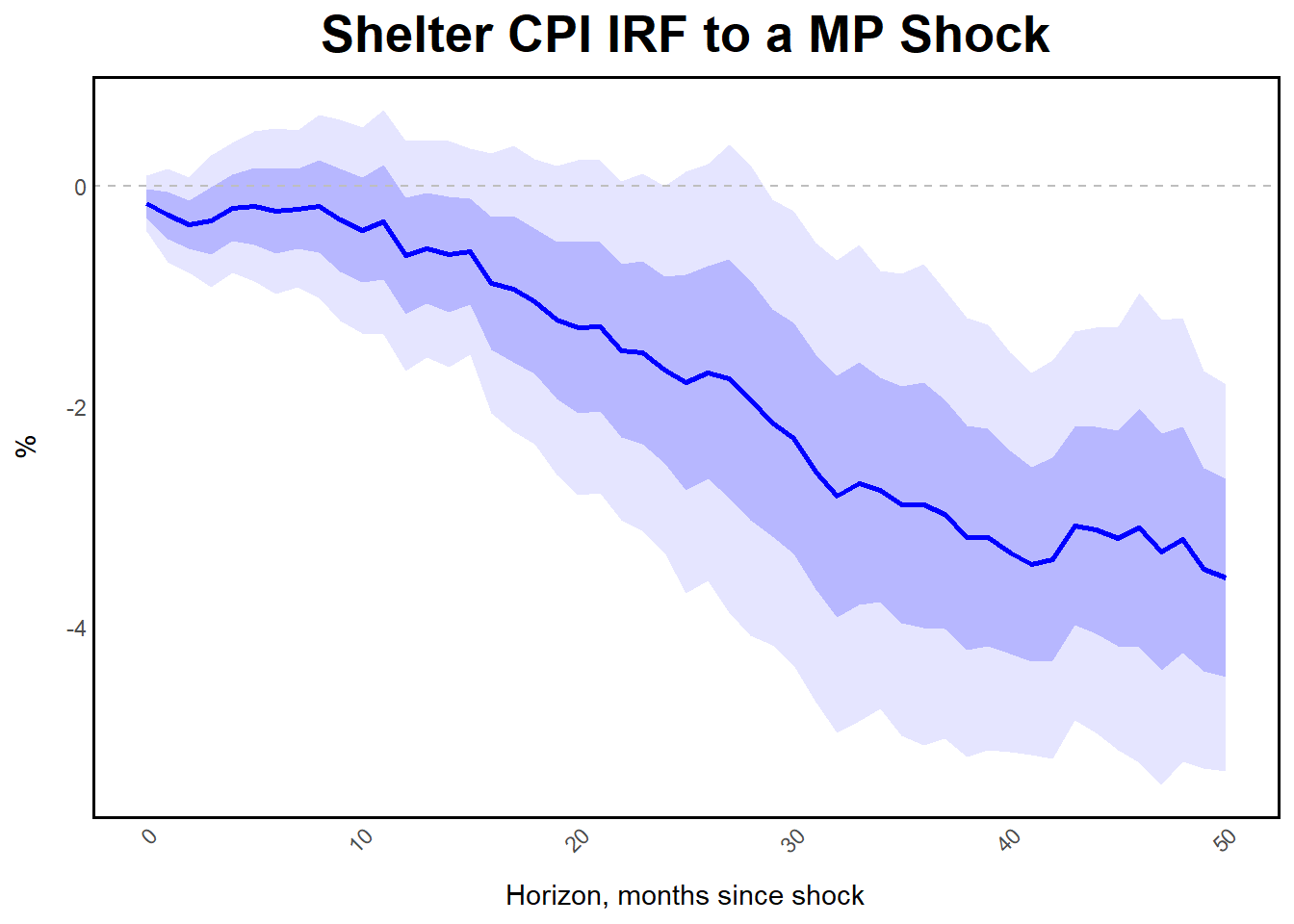

Replication of Figure 4 in Jordà (2024).

The figure illustrates the cumulative impulse response of shelter inflation (measured via the CPI) to a monetary policy shock, identified using high-frequency data from Bauer and Swanson (2023). Paper originally uses PCE inflation, although results are qualitatively similar. The shock isolates monetary policy changes while controlling for information effects. Traditional point-wise confidence intervals (Newey-West adjusted) as shaded bands are used.

Data

key <- "c27bf13d09598a184acdcb2ba94aa28f"

fredr_set_key(key)

cpi <- fredr_series_observations(series_id = "CUSR0000SAH1",

observation_start = as.Date("1969-01-31"),

observation_end = as.Date("2020-3-31"),

frequency = "m",

aggregation_method = "sum",

units = "lin")

cpi <- cpi %>%

rename(cpi = value) %>%

mutate(lcpi =log(cpi)) %>%

select(-series_id, -realtime_start, -realtime_end, -cpi, -date)

data <- haven::read_dta("sigband_shelterinf.dta")

data <- cbind(data, cpi)

data <- data %>%

dplyr::select(-mon_shock) %>%

rename(mon_shock = BSmonshock) %>%

filter(!is.na(mon_shock))Local Projection

Regress long-difference Shelter CPI with 12 lags of log CPI shelter, unemployment rate and federal funds rate.

# Set parameters

h <- 50 # Plot horizon

p <- 0.05 # Significance level of test

nwlag <- h # Newey-West lags

data <- data %>%

mutate(lpcepi_house = 100 * lpcepi_house) %>%

mutate(lcpi = 100*lcpi)

# Generate forward variables for LP regressions: Cumulative

for (i in 0:h) {

data[[paste0("lcpi_f", i)]] <- lead(data$lcpi, i) - lag(data$lcpi)

}

b_lpcepi_house_stir <- rep(NA, h + 1)

se_lpcepi_house_stir <- rep(NA, h + 1)

# Run Newey-West regressions and store coefficients and standard errors

for (i in 0:h) {

model <- lm(data[[paste0("lcpi_f", i)]] ~ mon_shock +

lag(data$lcpi, 1) + lag(data$lcpi, 2) + lag(data$lcpi, 3) +

lag(data$lcpi, 4) + lag(data$lcpi, 5) + lag(data$lcpi, 6) +

lag(data$lcpi, 7) + lag(data$lcpi, 8) + lag(data$lcpi, 9) +

lag(data$lcpi, 10) + lag(data$lcpi, 11) + lag(data$lcpi, 12) +

lag(data$stir, 1) + lag(data$stir, 2) + lag(data$stir, 3) +

lag(data$stir, 4) + lag(data$stir, 5) + lag(data$stir, 6) +

lag(data$stir, 7) + lag(data$stir, 8) + lag(data$stir, 9) +

lag(data$stir, 10) + lag(data$stir, 11) + lag(data$stir, 12) +

lag(data$urate, 1) + lag(data$urate, 2) + lag(data$urate, 3) +

lag(data$urate, 4) + lag(data$urate, 5) + lag(data$urate, 6) +

lag(data$urate, 7) + lag(data$urate, 8) + lag(data$urate, 9) +

lag(data$urate, 10) + lag(data$urate, 11) + lag(data$urate, 12),

data = data)

b_lpcepi_house_stir[i + 1] <- coef(model)["mon_shock"]

se_lpcepi_house_stir[i + 1] <- sqrt(diag(NeweyWest(model, lag = nwlag))["mon_shock"])

}

# Create a new data frame with the calculated confidence bands

data <- data.frame(

u1_lpcepi_house_stir = b_lpcepi_house_stir + se_lpcepi_house_stir,

d1_lpcepi_house_stir = b_lpcepi_house_stir - se_lpcepi_house_stir,

u2_lpcepi_house_stir = b_lpcepi_house_stir + qnorm(1 - p / 2) * se_lpcepi_house_stir,

d2_lpcepi_house_stir = b_lpcepi_house_stir - qnorm(1 - p / 2) * se_lpcepi_house_stir

)ggplot(data, aes(x = seq(0, h, 1))) +

geom_ribbon(aes(ymin = d2_lpcepi_house_stir, ymax = u2_lpcepi_house_stir), fill = "blue", alpha = 0.1) +

geom_ribbon(aes(ymin = d1_lpcepi_house_stir, ymax = u1_lpcepi_house_stir), fill = "blue", alpha = 0.2) +

geom_line(aes(y = b_lpcepi_house_stir), color = "blue", size = 1) +

geom_hline(yintercept = 0, linetype = "dashed", color = "gray") +

labs(x = "Horizon, months since shock", y = "%", title = "Shelter CPI IRF to a MP Shock") +

theme_minimal() +

theme(

plot.title = element_text(hjust = 0.5, size = 20, face = "bold"),

plot.subtitle = element_text(hjust = 0.5, size = 14, face = "italic", margin = margin(t = 10, b = 10)),

axis.text.x = element_text(angle = 45, hjust = 1),

panel.grid.major = element_blank(),

panel.grid.minor = element_blank(),

panel.border = element_rect(color = "black", fill = NA, size = 1),

axis.line = element_blank(),

axis.ticks.length = unit(-0.25, "cm"),

axis.title.x = element_text(margin = margin(t = 10)),

axis.title.y = element_text(margin = margin(r = 10)),

legend.position = "top",

legend.title = element_blank(),

legend.text = element_text(size = 12)

)