#from Functions import *

from scipy.interpolate import interp1d

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

import os

from datetime import datetime

import tkinter.filedialog

from datetime import timedelta

import math

import time

import calendar

from numba import jit

from sklearn.metrics import mean_squared_error

from statsmodels.tsa.api import VAR

import scipy

import statsmodels.tsa.stattools as ts

import statsmodels.tsa as tsa

import matplotlib.pyplot as plt

import numpy as np

import sklearn

from sklearn.metrics import mean_squared_error, r2_score

import statsmodels.api as sm

from datetime import datetime,timedelta

from statsmodels.tsa.stattools import adfuller

from numpy.linalg import cholesky

def Factor(Y, X_slow, n_factors, X_fast='None'):

#n_time = len(Y.index)

n_var = len(Y.columns)

if isinstance(X_fast,str)==True:

hist = Y.join(X_slow)

else:

hist = Y.join(X_slow).join(X_fast)

hist=hist.dropna(axis=0,how='any')

"step 1 - PCA on all observable variables"

x = np.mat(hist - hist.mean())

z = np.mat((hist - hist.mean())/hist.std())

D, V, S = calculate_pca(hist, n_factors + n_var)

Psi = np.mat(np.diag(np.diag(S - V.dot(D).dot(V.T))))

factors = V.T.dot(z.T).T

C = pd.DataFrame(data=factors, index=hist.index, columns=['C' + str(i+1) for i in range(n_factors+n_var)])

Loadings_C = calculate_factor_loadings(hist, C)

"step 2 - PCA on slow moving variables"

x = np.mat(X_slow-X_slow.mean())

z = np.mat((X_slow-X_slow.mean())/X_slow.std())

D, V, S = calculate_pca(X_slow, n_factors)

Psi = np.mat(np.diag(np.diag(S - V.dot(D).dot(V.T))))

factors = V.T.dot(z.T).T

F_minus = pd.DataFrame(data=factors, index=X_slow.index, columns=['F_minus' + str(i+1) for i in range(n_factors)])

Loadings_F_slow = calculate_factor_loadings(X_slow, F_minus)

"step 3 - C_t = b1*Y_t + b2*F_t"

X = Y.join(F_minus)

B = calculate_factor_loadings(C, X)

Lambda_y, Lambda_f = B[:,0:n_var], B[:,n_var:]

# F_t= Lambda_f^-1*(C_t-Lambda_y*Y_t)

F = Lambda_f.I.dot((np.mat(C).T - Lambda_y.dot(Y.T))).T

F = pd.DataFrame(data=F, index=X_slow.index, columns=['F' + str(i+1) for i in range(n_factors)])

return FactorResultsWrapper(C=C, Lambda_c=Loadings_C, F_minus=F_minus, F=F)

class FactorResultsWrapper():

def __init__(self, C, Lambda_c, F_minus, F):

self.C = C

self.Lambda_c = Lambda_c

self.F_minus = F_minus

self.F = F

def FAVAR(Factor, Y, lag):

hist = Y.join(Factor)

model=VAR(hist,missing='drop').fit(lag,trend='n')

return FAVARResultsWrapper(VAR=model)

class FAVARResultsWrapper():

def __init__(self, VAR):

self.VAR = VAR

def summary(self):

print(self.VAR.summary())

return

def predict(self, Factor, Y, step, freq='M', alpha=0.05):

hist = Y.join(Factor)

[forecast_mean,forecast_low,forecast_up] = self.VAR.forecast_interval(hist.values, step, alpha)

mean = np.concatenate((hist.values, forecast_mean), axis=0)

up = np.concatenate((hist.values, forecast_up), axis=0)

low = np.concatenate((hist.values, forecast_low), axis=0)

dates = pd.date_range(Y.index[0], periods=len(Y.index)+step,freq=freq)

mean = pd.DataFrame(data=mean[:,0:len(Y.columns)], columns=Y.columns.tolist(), index=dates)

low = pd.DataFrame(data=low[:,0:len(Y.columns)], columns=Y.columns.tolist(), index=dates)

up = pd.DataFrame(data=up[:,0:len(Y.columns)], columns=Y.columns.tolist(), index=dates)

return [mean,low,up]

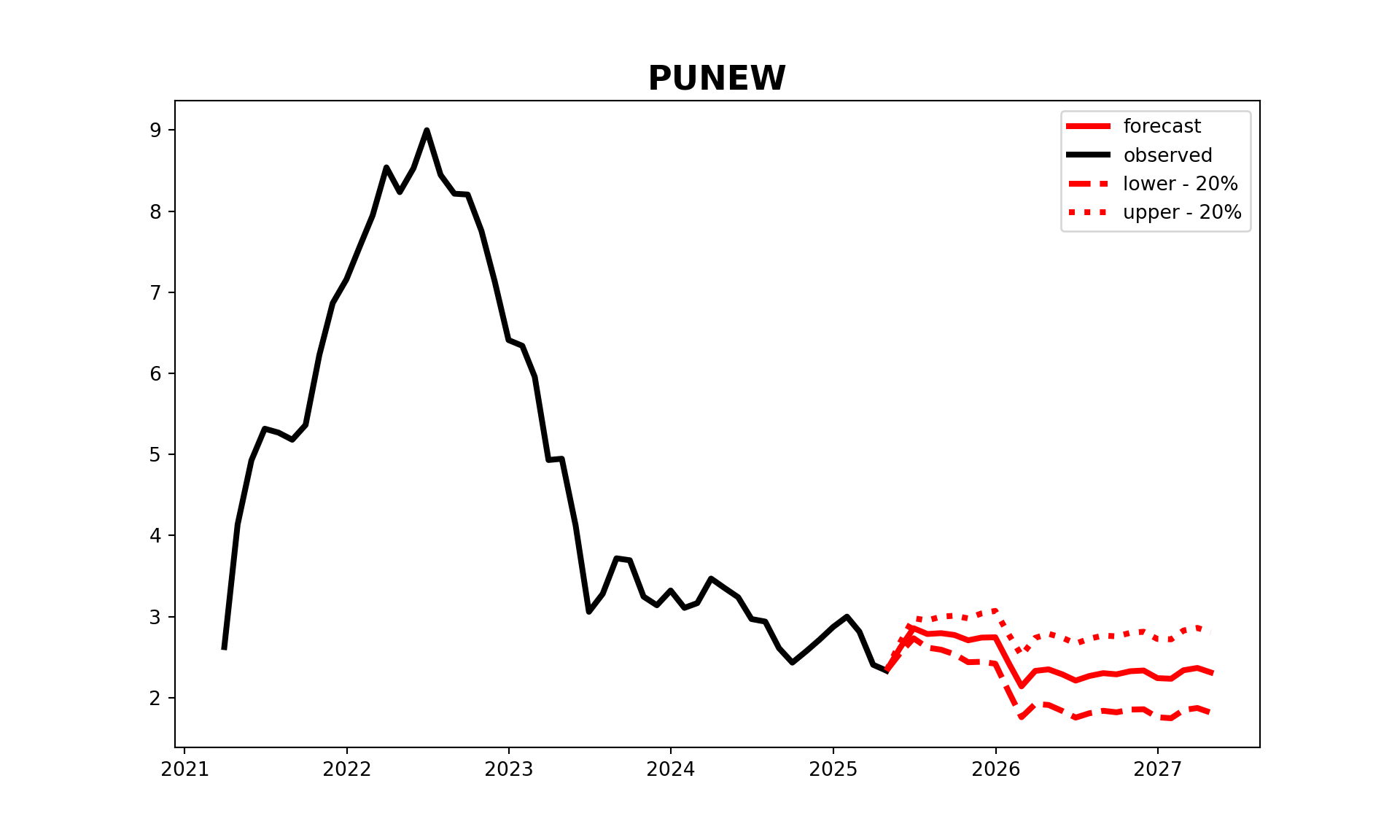

def predict_plot(self, Factor, Y, step, freq='M', alpha=0.05, figure_size=[18,12],line_width=3.0,font_size='xx-large', actural='None'):

mean, low, up = self.predict(Factor, Y, step, freq, alpha)

n_var = len(mean.columns)

n_act = len(Y.index)

plt.rcParams['figure.figsize'] = (figure_size[0], figure_size[1])

plt.rcParams['lines.markersize'] = 6

plt.rcParams['image.cmap'] = 'gray'

for i in range(n_var):

plt.figure()

plt.plot(mean.index[n_act-1:],mean.iloc[n_act-1:,i],color='r',label='forecast', linewidth=line_width)

plt.plot(mean.index[:n_act],mean.iloc[:n_act,i],color='k',label='observed',linewidth=line_width)

plt.plot(mean.index[n_act-1:],low.iloc[n_act-1:,i],color='r', linestyle = '--', label='lower - '+str(int(100-alpha*100))+'%',linewidth=line_width)

plt.plot(mean.index[n_act-1:],up.iloc[n_act-1:,i],color='r', linestyle = ':', label='upper - '+str(int(100-alpha*100))+'%',linewidth=line_width)

plt.legend()

if isinstance(actural,str)!=True:

plt.plot(mean.index[n_act-1:],actural.iloc[:,i],color='k',label='observed', linewidth=line_width)

plt.title(mean.columns[i], fontweight='bold', fontsize=font_size)

#plt.xlabel('Date')

#plt.ylabel('Value')

plt.show()

returnInflation Forecasting (Under validation)

Factor Augmented VAR for Inflation Forecasting in Python

Model, variable choice and variable transformation based on Bernanke (2005).

FAVAR

A Factor-Augmented Vector Autoregression (FAVAR) extends the traditional VAR model by incorporating latent factors that summarize information from a large dataset. Standard VAR models are limited by the small number of observed macroeconomic variables, which can lead to omitted variable bias. Bernanke, Boivin, and Eliasz (2005) introduced FAVAR to improve macroeconomic analysis, particularly in monetary policy studies. The model extracts unobserved factors from a large panel of economic indicators using techniques like Principal Component Analysis (PCA) or Kalman filtering, thus enhancing the information set available for forecasting and impulse response analysis.

First, a factor equation represents a large set of observed macroeconomic variables \(X_t\) as a function of latent factors \(F_t\) and a factor loading matrix \(\Lambda\), given by:

\[ X_t = \Lambda F_t + u_t. \]

Second, the VAR structure models the dynamic relationship between factors and a subset of observed macroeconomic variables \(Y_t\), following: \[ \begin{bmatrix} F_t \\ Y_t \end{bmatrix} = A_1 \begin{bmatrix} F_{t-1} \\ Y_{t-1} \end{bmatrix} + \dots + A_p \begin{bmatrix} F_{t-p} \\ Y_{t-p} \end{bmatrix} + \varepsilon_t. \] Here, \(A_i\) are coefficient matrices and \(\varepsilon_t\) is the error term. This structure enables a richer characterization of macroeconomic shocks and policy effects.

We base the excercise on the mentioned paper, particulary variable characterization in either fast or slow variables.

#from FactorAugmentedVAR import *

#from Functions import *

from datetime import *

import warnings

import pandas as pd

warnings.filterwarnings('ignore')

# Data Import

file_name ='favardata.xlsx'

sheet_name ='Sheet1'

Temp = pd.read_excel(file_name, sheet_name)

vintage_transformed = Temp.iloc[:,1:]

vintage_transformed.index = Temp.iloc[:,0]

#Data Interpolation

vintage_intrpl = DataInterpolation(vintage_transformed[1:], 0, len(vintage_transformed.index), 'slinear').dropna(axis=0,how='any')

# Factor Calculation

factor = Factor(Y=pd.DataFrame(vintage_intrpl.iloc[:,0]),

X_slow=vintage_intrpl.iloc[:,1:54],

n_factors=3,

X_fast=vintage_intrpl.iloc[:,54:])

#factor.C.plot()

#factor.F.plot()

favar = FAVAR(Factor=factor.F, Y=pd.DataFrame(vintage_intrpl.iloc[:,0]), lag=12)

#favar.VAR.summary()

mean, low, up = favar.predict(Factor=factor.F[-12:], Y=pd.DataFrame(vintage_intrpl.iloc[-12:,0]), step=24)

favar.predict_plot(Factor=factor.F[-12:], Y=pd.DataFrame(vintage_intrpl.iloc[-50:,0]), step=24, freq='M', alpha=0.8, figure_size=[10,6],line_width=3.0,font_size='xx-large', actural='None')

Without differencing between slow/fast variables (k = 3)

slowvars <- reduce(dataframes_list, full_join, by = "date")

df <- full_join(slowvars, vars, by = "date")

df <- drop_na(df)

X <- df %>% dplyr::select(-date, -PUNEW)

Y <- df %>% dplyr::select(PUNEW)

K <- 3

h <- 25

X <- as.matrix(X)

Y <- as.matrix(Y)

fore_FAVAR <- function(X, Y, K, y_name, h, y=Y[,y_name], use_VAR = F){

library("tidyverse")

library("forecast")

library("vars")

library("lmtest")

start <- start(X)

frequency <- frequency(X)

X = X[1:length(y),]

Y = Y[1:length(y),,drop=FALSE]

N = dim(X)[2]

M = dim(Y)[2]

T = dim(X)[1]

# extract PC from X

XtX = t(X) %*% X

spectral_decomposition <- eigen(XtX)

eig_vec <- spectral_decomposition$vectors

eig_val <- spectral_decomposition$values

lam <- 1/sqrt(N) * eig_vec[,(1:K)]

Fr <- data.matrix(X) %*% lam

# FAVAR with clean factors

if(use_VAR == F){

Y_for_VAR = cbind(Fr, Y)

factor_names = paste('factor', 1:K)

colnames(Y_for_VAR)[1:K] <- factor_names

}

else

Y_for_VAR = Y

Y_for_VAR <- ts(Y_for_VAR, start = start, frequency = frequency)

VARselect(Y_for_VAR)

p = VARselect(Y_for_VAR)$selection[1] # according AIC

var <- VAR(Y_for_VAR, p)

y_hat <- forecast::forecast(var, h=h)

return(y_hat)

}

test <- fore_FAVAR(X = X, Y = Y, K = K, h = h)

test$forecast$PUNEW[3]$mean

Time Series:

Start = 386

End = 410

Frequency = 1

[1] 2.491944 2.527905 2.536481 2.599700 2.588145 2.542168 2.503306 2.503406

[9] 2.508942 2.513279 2.521223 2.533958 2.533297 2.540996 2.552216 2.558449

[17] 2.567631 2.583297 2.594843 2.605121 2.616182 2.624944 2.629688 2.633462

[25] 2.637104