library(bsvars)endog <-as.matrix(endog)exog <-as.matrix(exog)specification <- specify_bsvar$new(data = endog,exogenous = exog,p =4)set.seed(123)# run the burn-inburn_in =estimate(specification, 10000)

**************************************************|

bsvars: Bayesian Structural Vector Autoregressions|

**************************************************|

Gibbs sampler for the SVAR model |

**************************************************|

Progress of the MCMC simulation for 10000 draws

Every draw is saved via MCMC thinning

Press Esc to interrupt the computations

**************************************************|

# estimate the modelposterior =estimate(burn_in, 50000)

**************************************************|

bsvars: Bayesian Structural Vector Autoregressions|

**************************************************|

Gibbs sampler for the SVAR model |

**************************************************|

Progress of the MCMC simulation for 50000 draws

Every draw is saved via MCMC thinning

Press Esc to interrupt the computations

**************************************************|

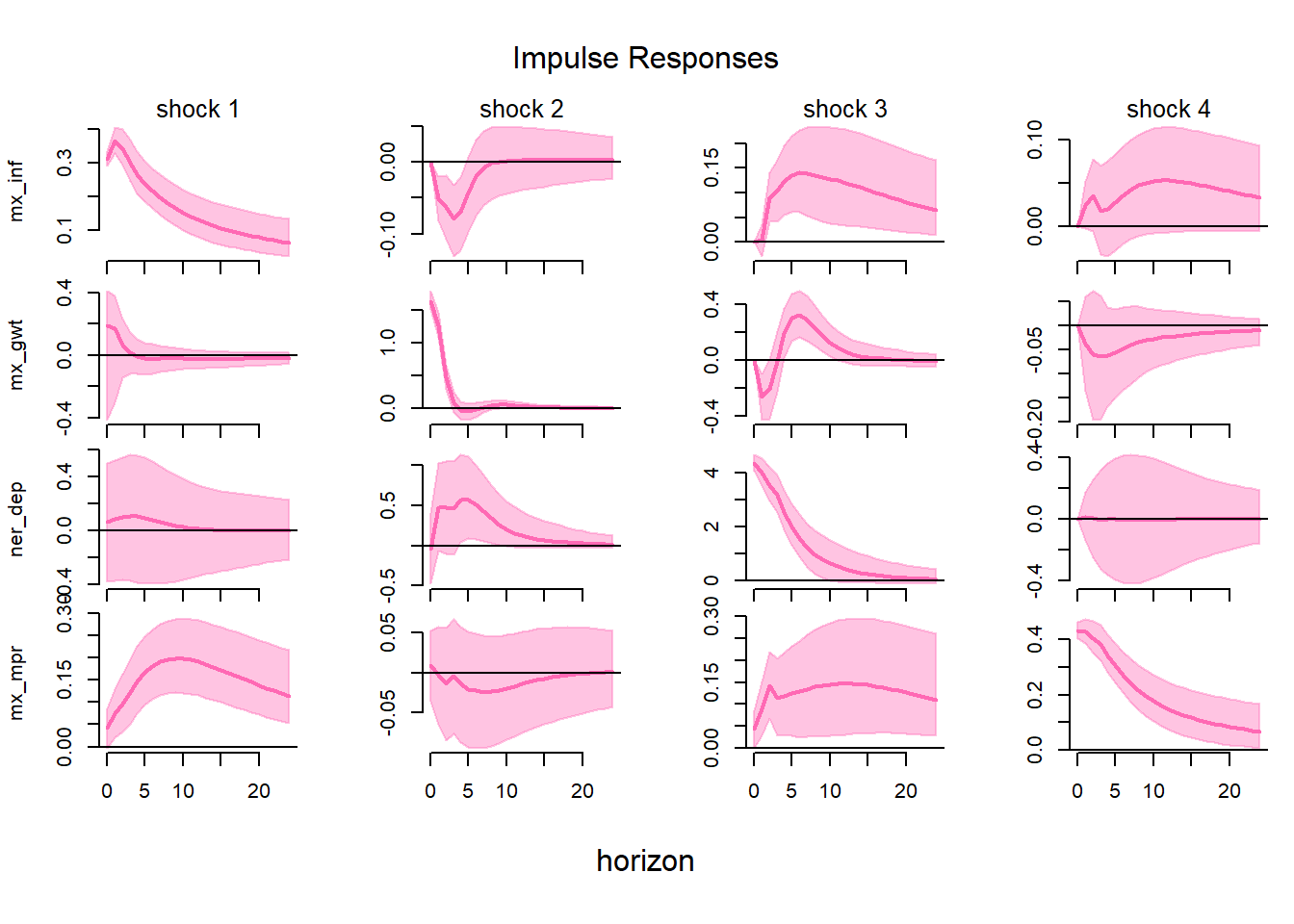

p <-compute_impulse_responses(posterior, horizon =24) plot(p)